The question of what is the minimum CIBIL score for a personal loan approval is perhaps the most critical determinant for any applicant seeking unsecured finance in India. Your CIBIL Score is not just a three-digit number; it is a validated financial passport that dictates whether your application is approved, how quickly the funds are disbursed, and, most importantly, the Annual Percentage Rate (APR) you will pay over the loan’s tenure.

As personal loans are unsecured (no collateral is required), lenders rely almost entirely on this score to evaluate your creditworthiness and repayment risk. While there is no single, universally mandated score, the benchmark for seamless approval and preferential rates is firmly established. This is why understanding the minimum credit score for a loan is essential.

This comprehensive guide delves deep into the score requirements, explains how lenders evaluate your profile in light of latest RBI Digital Lending Directions, and provides actionable steps to ensure your credit score not only meets the minimum threshold but positions you for the best possible loan terms.

Table of Contents

ToggleUnderstanding Your CIBIL Score: The Gateway to Loan Approval

Before addressing the specific numerical requirement, it is essential to understand the foundation. CIBIL, or Credit Information Bureau (India) Limited, is India’s leading credit information company and one of the four RBI-licensed Credit Information Companies (CICs). The CIBIL Score is a three-digit number ranging from 300 to 900 that summarises your entire credit history, including your borrowing and repayment behaviour across various credit products (credit cards, home loans, auto loans, etc.)

A higher score indicates a responsible borrower with a strong history of timely repayments, while a lower score signals a higher risk of default to lenders.

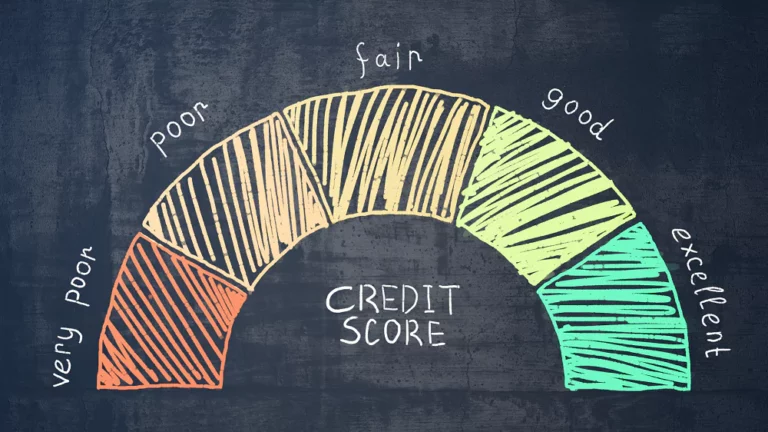

CIBIL Score Ranges and Their Impact on Personal Loan Eligibility

Lenders categorize applicants based on their CIBIL score range, which directly impacts their decision-making process for your personal loan application. The CIBIL score range for a loan is a key risk indicator.

CIBIL Score Range | Credit Health Classification | Likelihood of Personal Loan Approval | Expected Loan Terms |

750 – 900 | Excellent / Prime | Very High (Fastest approvals and higher limits) | Lowest interest rates, highest loan amounts, flexible tenure. |

700 – 749 | Good / Acceptable | High | Favourable interest rates, likely approval, standard terms. |

650 – 699 | Fair / Marginal | Moderate to Low | Approval possible, but often with higher interest rates and stricter terms. |

600 – 649 | Below Average / Subprime | Challenging | Limited lenders, significantly higher interest rates, small loan amounts. Secured products (like a gold loan) are often preferred. |

300 – 599 | Poor / High Risk | Extremely Low (Likely Rejection) | Approval is highly unlikely for unsecured loans. Focus on rebuilding credit with secured products. |

-1 to 0 (NA/NH) | No History / Not Applicable | Challenging | Approval depends on other factors (income, job stability) but may result in limited loan amount or require a co-applicant. |

What is the Minimum CIBIL Score Required for a Personal Loan?

While the absolute technical minimum CIBIL score for a personal loan is often considered 600 (as scores below this generally lead to automatic rejection), the practical minimum CIBIL score required for a personal loan approval from most major banks and regulated NBFCs is significantly higher.

- The Golden Standard: A CIBIL Score of 750 or above is universally recognized as the ideal or “good CIBIL score for a personal loan.” Applicants in this bracket are viewed as low-risk and are heavily sought after by lenders.

- The Functional Minimum: The functional or starting minimum credit score for loan that allows you to realistically apply for an unsecured personal loan with a reasonable chance of approval is generally 680 to 700.

Lender-Specific Minimum CIBIL Score Expectations (Post-2025 RBI Norms)

The minimum CIBIL score for loan approval is not static and varies based on the lender’s risk appetite, the applicant’s profile (salaried vs. self-employed), and adherence to new risk-weighted norms mandated by the RBI.

Lender Type | Typical Minimum CIBIL Score Expectation | Notes on Approval |

Major Public/Private Banks | 750+ (Often a hard cut-off) | Highly rigid. They prioritize low-risk profiles, especially given the higher risk weights on unsecured loans mandated by RBI. |

Regulated NBFCs (Non-Banking Financial Companies) | 700+ (Flexible down to 650 for high-income/stable employees) | More flexible, especially if the applicant has high and stable monthly income and a low Debt-to-Income (DTI) ratio. |

Digital Lenders / Fintech Platforms | 650+ (May consider lower scores like 600-649) | Often use alternate data scoring models beyond CIBIL, but interest rates and processing fees will be significantly higher due to the elevated risk. Ensure they are RBI-regulated entities. |

Key Takeaway: If your CIBIL score is below 700, focus on regulated NBFCs like Zype, which is a regulated NBFC, or Fintech platforms that are more risk-tolerant. If your score is 750 or above, major banks will offer the most competitive interest rates.

How Your CIBIL Score Impacts Personal Loan Terms: The Cost of Borrowing

The importance of the CIBIL score extends far beyond simple eligibility. It fundamentally determines the cost of borrowing, making a higher score a financially intelligent goal.

CIBIL Score and Interest Rate (APR)

Lenders use a system called risk-based pricing. A higher CIBIL score implies lower credit risk, which directly translates to a lower Annual Percentage Rate (APR) offered on the personal loan.

- High Score (750+): You can access the lowest advertised interest rates (often starting from 9.99% – 13.00% as of late 2025, subject to the prevailing repo rate) [Citation 3: Industry Benchmarks/NBFC Rate Disclosures, Nov 2025].

- Moderate Score (650-700): You will typically be offered interest rates that are 4% to 8% higher than the prime rates (potentially 15% – 22% or more).

Compliance Note: Key Fact Statement (KFS)

Under the RBI’s Digital Lending Directions (2025), all regulated entities (Banks/NBFCs) must provide a clear Key Fact Statement (KFS) to the borrower for every loan, detailing the Annual Percentage Rate (APR), all fees (processing, insurance, etc.), repayment schedule, and penalties upfront before sanction. This ensures full transparency regarding the total cost of the loan, especially for applicants with lower scores who face higher rates.

CIBIL Score | Interest Rate (Approx. APR) | Monthly EMI (₹5 Lakh, 5 years) | Total Interest Paid |

780 | 12.5% | ₹11,248 | ₹1,74,880 |

680 | 19.0% | ₹12,853 | ₹2,71,180 |

In this scenario, a lower score of 680 costs the borrower over ₹96,000 more in total interest over the life of the loan. This clearly illustrates why securing the highest score possible is crucial for long-term financial health.

CIBIL Score and Loan Tenure/Amount

A strong CIBIL score also influences two other crucial loan terms:

- Loan Amount: Lenders are more comfortable offering a higher loan up to ₹2 lakhs to a borrower with a 750+ score, as their risk of default is negligible. A low score applicant may be capped at a much smaller amount (e.g., ₹1-₹5 lakhs) and may be scrutinized more strictly against the prudent limit on the loan amount set by the lender.

- Loan Tenure: High-score applicants can often negotiate longer repayment tenures (up to 5-7 years) which reduces the monthly EMI burden, while low-score applicants may be restricted to shorter tenures to minimise the lender’s risk exposure.

Factors that Affect Your CIBIL Score

Key Influences on Your Credit Score You Should Know

Understanding what impacts your CIBIL score can help you maintain a healthy credit profile and improve your loan approval chances.

Timely EMI Payments

Making your EMI payments on time boosts your CIBIL score by reflecting positive credit behaviour. Late or missed EMIs negatively impact your score.

Credit Utilisation Ratio

High credit card utilisation on a regular basis can lower your credit score. Maintaining a low utilisation ratio helps keep your score healthy.

Multiple Loan Applications

Applying for loans or credit cards with multiple lenders simultaneously may reduce your score, as it signals credit-hungry behaviour.

Errors in CIBIL Report

Mistakes or inaccuracies in your free CIBIL report can adversely affect your score, so regular checks are important.

Monitor Your Credit Score Regularly

Stay informed and take proactive steps to maintain or improve your CIBIL score for better financial opportunities.

Checking Your CIBIL Score: Step-by-Step Guide

Checking your score is a crucial preliminary step before applying for any loan. Importantly, checking your own score is considered a soft inquiry and does not negatively affect your CIBIL Score.

- Free Report Access: As per RBI guidelines, you are entitled to one free full Credit Report (including the CIBIL Score) every calendar year from each of the four credit bureaus.

- Verify and Authenticate: Access your report through the official TransUnion CIBIL website or a partner NBFC/Bank after providing mandatory details like your PAN Card number and completing OTP authentication.

- Review the Credit Information Report (CIR): Scrutinise the report for any errors, such as:

- Loan accounts or credit cards you never took.

- Incorrectly marked ‘Closed’ accounts that are still showing as ‘Open’.

- Incorrect payment status (e.g., showing a payment as ‘Delayed’ when it was ‘On Time’).

- Dispute Errors Immediately: If errors are found, raise a dispute immediately with CIBIL. The RBI mandates a clear and time-bound grievance redressal process by credit bureaus and lenders

Proven Strategies to Improve Your CIBIL Score Quickly

If your score is currently below the preferred range and you are wondering how much CIBIL score required for a personal loan approval you need, implement these strategies immediately.

- Prioritise Payments on Time (The 35% Rule): This is the single most important factor. Set up auto-pay for all EMIs and credit card bills. Note: Due to RBI’s updated credit reporting directions, positive changes like timely payments will reflect faster than before.

- Drastically Lower Your Credit Utilisation (The 30% Rule): Pay down credit card debt aggressively. Aim to keep your outstanding balance below 30% of your total credit limit. Strategic Move: Consider requesting a credit limit increase. This lowers your CUR without increasing your debt.

- Limit Hard Inquiries: Do not apply to multiple lenders simultaneously hoping for approval. This lowers your score by a few points for each inquiry. Instead, use eligibility checkers offered by lenders (which use a soft inquiry) to determine your chance of approval before making a formal application.

- Settle Old Debts: If you have written-off or settled accounts, work to clear them. A ‘Settled’ status is better than a ‘Written Off’ status, but clearing the debt entirely is best.

Conclusion: The Path to the Lowest Cost of Borrowing

Securing a personal loan with favourable terms hinges almost entirely on meeting the practical minimum CIBIL score for loan eligibility, which sits at 750 and above for prime access. While scores as low as 650 may still secure funding, the borrower will inevitably face significantly higher costs, longer processing times, and potentially stricter terms, especially under the current 2025 RBI risk-weighted lending norms.

By treating your CIBIL score as a vital financial asset, consistently paying on time, keeping credit utilization low, and monitoring your Credit Information Report (CIR) diligently, you position yourself not just for loan approval, but for the lowest interest rates available in the market. This disciplined approach ensures that your next personal loan is not only approved quickly but is the most cost-effective borrowing decision possible.

YMYL & RBI Compliance Mandatory Disclaimer

This page is provided for informational purposes regarding unsecured personal loans, specifically the minimum CIBIL score for personal loan.

- Zype is a digital lending platform partnered with regulated Non-Banking Financial Company (NBFC). All loans are processed and sanctioned by the partner NBFC in strict compliance with the Reserve Bank of India (RBI) Fair Practices Code and Digital Lending Guidelines.

- Borrower Disclosures: The final terms, including the Annual Percentage Rate (APR), total loan cost, and detailed fees, will be explicitly and transparently disclosed to you in the Key Fact Statement (KFS) before the loan sanction, as mandated by the RBI Digital Lending Guidelines.

- Responsible Borrowing: Personal loans are subject to credit risk. Failure to repay installments may negatively affect your credit bureau score (CIBIL score). You must always borrow only what you can comfortably afford to repay.

Frequently Asked Question

What Happens If I Have No Cibil Score (NA or NH)?

A score of NA (Not Applicable) or NH (No History) means you are new to credit and have not taken any loans or credit cards yet. While technically you meet the “minimum CIBIL score for a loan” criteria (as there is no poor score), most traditional banks will be hesitant to approve an unsecured personal loan without any credit data. In this scenario:

- The Best Strategy: Get a secured credit card or a small secured loan (like a gold loan) first. Use it responsibly for 6-12 months to build a score above 750 before applying for an unsecured personal loan.

- Options: You may need to apply to an NBFC or digital lender who may approve the loan based purely on your high income, job stability, and employer profile, but be prepared for a lower loan amount and potentially higher interest rates.

Can I Get A Personal Loan With A Cibil Score Below 650?

Getting a traditional, unsecured personal loan from major banks or top-tier NBFCs is extremely difficult with a CIBIL score below 650. Options may include:

- Secured Loans: Applying for a Gold Loan or Loan Against Property, where the asset acts as collateral, making the CIBIL score less critical.

- Joint Application: Applying with a co-applicant who has an excellent credit score (750+).

- P2P Lenders: Exploring Peer-to-Peer lending platforms, which often have higher risk tolerance but charge exorbitant interest rates (often 25% or more) and should be approached with caution. Always verify the RBI registration status of any P2P platform.

Does My Income Or Job Stability Override A Low CIBIL Score?

Income and job stability are secondary eligibility criteria but are crucial supporting factors. While high income (e.g., ₹1.5 lakh per month) and a secure job at an MNC or PSU can certainly improve your chances, they rarely override a very poor CIBIL score (below 600-650) for unsecured loans. Lenders prefer a responsible borrower over a rich but financially erratic one. However, if your score is borderline (680-700), a high income profile can be the deciding factor for approval, especially if your Debt-to-Income (DTI) ratio is low (ideally below 40%).

How Long Does It Take To Improve A Cibil Score From 600 To 750?

Significant improvement from 600 to 750 typically takes 6 to 12 months of highly disciplined credit behaviour. Key actions that reflect quickly (within 3-6 months) include:

- Clearing outstanding credit card debt to bring the Credit Utilisation Ratio (CUR) below 30%.

- Making all existing loan EMIs and credit card payments 100% on time during this period.

- Correcting any errors in your Credit Information Report (CIR) via dispute resolution.

What Is The Difference Between A Soft Inquiry And A Hard Inquiry?

- Soft Inquiry: Occurs when you check your own credit score (e.g., via the CIBIL website or Zype’s checker), or when a bank pulls your score for pre-approved offers (marketing purposes). It is invisible to other lenders and does not affect your score.

- Hard Inquiry: Occurs when you formally apply for a new loan or credit card, and the lender pulls your report to evaluate the application. Too many hard inquiries in a short time signal high risk and can temporarily lower your score by a few points.