What is a Good Credit Score: Range, Factors & Benefits

From getting approved for a small ticket loan of ₹3,000 to a full-fledged home loan, your credit score plays a very crucial role in it.

Your credit score shows the lender how safe or risky you are as a borrower. Based on this information, they decide if you are eligible for their credit product or not and what is the maximum credit limit you should get. In this blog, we’ll learn everything you should know about the credit score.

Table of Contents

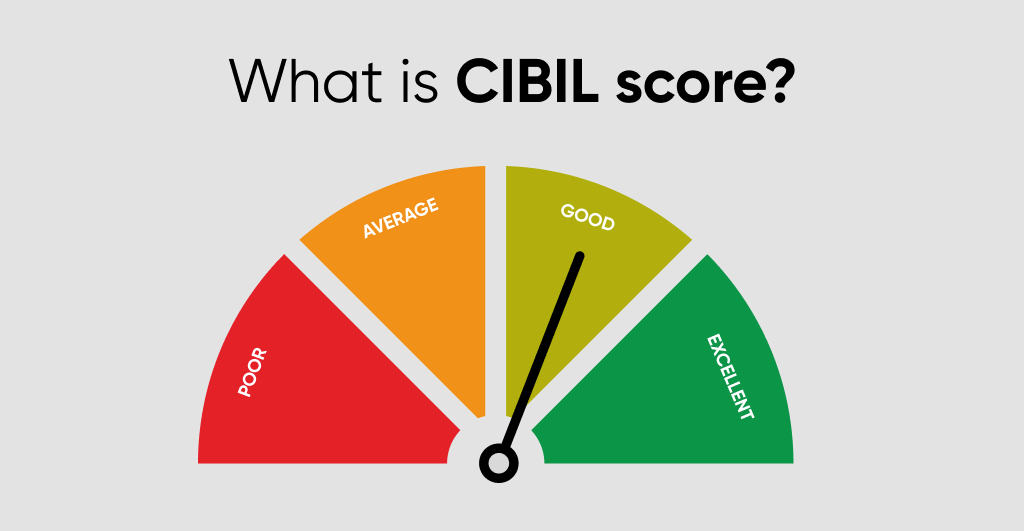

ToggleWhat is CIBIL score?

The Credit Information Bureau India Limited (CIBIL) is a bureau authorized by the RBI that generates the credit score based on the credit report and repayment behavior. That credit score is called a CIBIL score. They follow a score range of 300-900.

The CIBIL Score is a three-digit number, ranging from 300 to 900, that shows your creditworthiness. It lets the lender gauge your credit behaviour. When you borrow money and repay it on time, you build a good credit score. This credit score is captured in your CIBIL Score. The higher your score, the more responsible you appear, making it easier for you to get loans and credit cards on good terms.

What is a Good Credit Score?

A good credit score usually ranges between 670 – 739, showing that you’ve been responsible with credit. Scores of 740 – 799 are considered very good, while 800+ is excellent. A higher score improves your chances of quick loan approvals, better interest rates, and access to higher credit limits. In short, it’s your financial credibility number that makes borrowing easier and cheaper.

| Cibil Score Range | Rating |

| < 650 | Poor |

| 650 – 699 | Average |

| 700 – 749 | Good |

| 750 – 799 | Very good |

| > 799 | Excellent |

Anything above 700 is considered as good CIBIL score. This increases your chances of getting a higher credit amount, lower interest rates, and many other benefits.

Read More: What is CRIF? Difference Between CIBIL & CRIF Score

Benefits of Maintaining a Good CIBIL Score

Your CIBIL score is so much more than a three-digit number. It can help your loan application in the following ways:

1. Instant Loan Approvals

A good CIBIL score is one of the key indicators of a low-risk borrower who can be trusted with credit. When you show a history of responsible borrowing and timely repayments, you are more likely to get approved for loans faster. This is because a high credit score gives the loan provider confidence in your ability to repay the loan.

Read More: How to Get Perfect 900 Credit/CIBIL Score?

2. Quicker Disbursements

If you have a good CIBIL score, it can help speed up the process of disbursal after you are approved for a loan. This is because you would become a priority customer for the lender because of good repayment behavior.

3. Higher Credit at Lower Interest Rates

High-ticket loans such as home loans, car loans and personal loans can have a high interest rate. But when you have a good CIBIL score, you give yourself an added advantage of being able to avail these high-ticket loans at lower interest rates. This will significantly help you borrow money at a lower cost.

What is the Range of Cibil Score?

Your CIBIL score typically ranges between 300 and 900. The higher your score, the better your chances of loan approval at favorable terms. Knowing where you fall in this range helps you understand your credit health and plan improvements if needed.

Score Band | Category | Significance & Impact on Loan |

300 – 549 | Poor | Very high risk of default. Loan applications are mostly rejected. Even if approved, interest rates will be extremely high. |

550 – 649 | Fair | Considered subprime. Lenders still may see you as risky. You may get loans, but at higher interest rates and with stricter terms. |

650 – 699 | Average | Shows moderate credit discipline. Some lenders may approve loans, but interest rates won’t be the best. |

700 – 749 | Good | Indicates responsible credit use. Most lenders are comfortable lending, with reasonable interest rates and better approval chances. |

750 – 799 | Very Good | Strong repayment history; higher chances of quick approvals, better loan offers, and lower interest rates. |

800 – 900 | Excellent | Excellent credit behaviour; best loan terms, fastest approvals, higher limits, and lowest interest rates. |

Factors that Affect CIBIL Score

Your three-digit CIBIL score is calculated after keeping many factors in mind:

1. Repayment History

The way you wouldn’t want to lend money to that friend who never pays you back, a lender would never want to give credit to people who make late payments on their EMIs, credit card bills or default on their repayments. Your repayment history is a significant contributor to your credit score. Late payments, defaulting on loans, and paying only the minimum amount are signs of a bad repayment history which reflects negatively on the CIBIL score.

2. Credit Mix

Credit Mix means having a balanced amount of secure and unsecured loans such as credit cards, car loans and more. A good credit mix is important for maintaining a good credit score. A diverse mix of loans indicates you can manage different types of credit which can help you improve your CIBIL score.

3. Multiple Enquiries

Whenever you apply for a loan, the credit provider assesses your credit profile which is known as a credit enquiry. Having too many enquiries in a short period of time can have a negative impact on your credit score. Hence, it is important to avoid applying credit cards and loans in a short period of time as this may have a negative impact on your profile.

4. Credit Utilization

Credit utilization is the total credit that you use out of the total amount of credit across all your cards. Having a high credit utilization can negatively affect your credit score. Hence the best practice to maintain a good CIBIL score is to ensure that your credit utilization is not more than 30% on individual cards.

What is CIBIL Report?

CIBIL report, also known as Credit Information Report or CIR, is the report of an individual’s credit repayment history of all credit cards and loans. CIBIL report, also known as Credit Information Report or CIR, is the report of an individual’s credit repayment history of all credit cards and loans.

Your CIBIL report has details of all your credit accounts like loans, overdrafts and credit cards. A CIBIL report makes it easier for lenders to assess your creditworthiness since it shows how you’ve managed your debt in the past, and whether you made repayments on time.

Read More: How to download CIBIL report

How Does Cibil Compute Your Credit Score?

Your CIBIL Score is calculated based on your financial habits. Every loan you take, every EMI you pay (or miss), and even how often you apply for credit leaves a mark on your record. CIBIL collects and analyzes this data to create your score, which acts like a report card of your creditworthiness. Understanding how it’s computed can help you take the right steps to maintain or improve it.

- Payment History (35%)

This is the most important factor. Timely repayment of EMIs and credit card bills boosts your score, while delays or defaults lower it. - Credit Utilization (30%)

How much credit you use compared to your total limit. Keeping usage below 30% of your limit shows financial discipline. - Credit Mix & Duration (15%)

Having a healthy mix of secured loans (like home loans) and unsecured loans (like personal loans or credit cards), along with longer credit history, strengthens your score. - Number of Credit Inquiries (10%)

Each time you apply for a loan/credit card, lenders make a “hard inquiry.” Too many such inquiries in a short span can hurt your score. - Outstanding Debt (10%)

The total amount you still owe across loans and cards also affects your score. Lower outstanding balances equals a better score.

Tips to Maintain a Good CIBIL Score

You can improve your CIBIL score by practicing these 5 simple steps:

1. The best practice for maintaining a good CIBIL score is to make your repayments on time. An easy way of going about this is by setting auto-debit for all your repayments.

2. Ensure your credit utilization doesn’t exceed 50 percent. The best practice is to make sure your utilization is around 25-30%.

3. Maintain a healthy credit mix and make sure you’re repaying all your loans on time.

4. Keep a check on the number of credit enquiries you make. Applying for too many loans and credit cards at once can increase the total number of inquiries which can negatively affect your score.

5. Make it a habit to review your CIBIL report at regular intervals. This will help you avoid any form of discrepancies and ensure that there are no errors in your report.

In Conclusion

Maintaining a good CIBIL score comes with advantages like instant loan approvals, faster disbursals, higher amounts, and low interest rates, and is also a sign of good financial health and good personal finance habits.

Frequently Asked Question

What Is A Cibil Score Range?

A CIBIL score ranges between 300 and 900. It reflects the creditworthiness of the borrower. Individuals with scores above 700 are considered responsible borrowers.

What Is The Minimum And Maximum Cibil Score In The Range?

The lowest CIBIL score is 300, and the highest is 900. You should always maintain a good credit score so you can enjoy better credit and financial opportunities.

Can Errors In The Credit Report Affect The Cibil Score Range?

Errors in your credit report can affect your CIBIL score. Common errors include incorrect personal information, duplicate accounts, incorrect loan balances, etc. You can contact the credit bureau to get these mistakes resolved.

Are There Different Cibil Score Ranges For Different Types Of Loans?

The CIBIL score ranges from 300 and 900. Loan companies have different criteria and CIBIL score requirements for different types of loans. It also varies from lender to lender.

How Does A Good Cibil Score Affect My Loan Or Credit Card Application?

Individuals with high CIBIL scores are perceived as less risky borrowers. As a result, it increases your chances of approval, gives you higher credit limits and makes it possible to get loans at low-interest rates.

What Is A Good Cibil Score Range?

A good CIBIL score typically ranges from 750 to 900. This score range indicates a strong credit history and suggests that you are a responsible borrower, making it easier to get loans and credit cards with favourable terms.

What Are The 5 Levels Of Credit Scores?

A credit score between 300–850 is usually divided into five levels: Poor (300–579), Fair (580–669), Good (670–739), Very Good (740–799), and Exceptional (800–850). Higher scores show stronger creditworthiness, improving your chances of faster loan approvals and lower interest rates.

How Do I Increase My Cibil Score?

The most common ways to increase your CIBIL score is by clearing outstanding dues, making timely payments, and reducing your credit utilization below 30%. Disputing errors on your report can also lead to an immediate boost.

How Much Cibil Score Is Required For EMI?

A 700 CIBIL Score is considered fair. It may get your loan approved, but often with higher interest rates or stricter terms. To access better financial opportunities, aim for 750 or above, which is generally seen as very good. With a stronger score, you’re more likely to enjoy benefits like lower interest rates, faster approvals, and higher credit limits—for example, even a generous limit on your Instant EMI Card.